Japan remains one of the most strategically important markets in the global economy. As the world’s fourth-largest economy, a hub of advanced manufacturing, and a cornerstone of global supply chains, it continues to exert outsized influence far beyond its borders. For Western companies operating in materials, industrial systems, energy, healthcare, and advanced technology, Japan is not an optional market. It is a reference market.

What has changed is not Japan’s relevance, but how growth is created and captured.

Japan’s economy is increasingly defined by deliberate, long-dated capital allocation toward energy security, industrial resilience, automation, and institutional capacity. Growth is not driven by consumer expansion or rapid market churn, but by structural commitments made by corporations, ministries, and public institutions to sustain output, reliability, and quality under tightening constraints.

For Western CEOs, this distinction matters. Japan rewards companies that align with how capital is deployed and decisions are made. It penalises those that expect fast cycles, discretionary purchasing behaviour, or regional “Asia-Pacific” templates to translate cleanly.

The opportunity in Japan is therefore not about speed or scale. It is about positioning for durable demand where spend per unit of output is rising structurally, and where customer relationships, once established, are exceptionally resilient.

Japan is often assessed through headline indicators such as GDP growth or consumer sentiment. These metrics are poor guides to strategic opportunity.

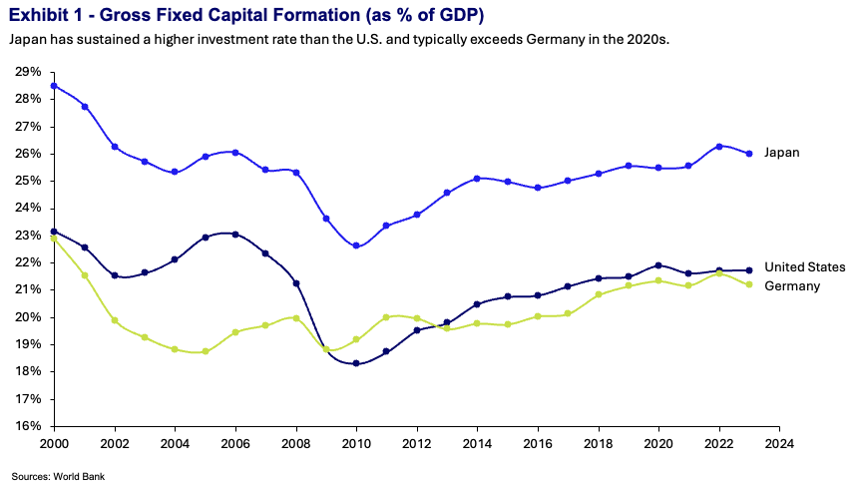

A more revealing lens is capital allocation. Despite modest headline GDP growth, Japan has consistently maintained gross fixed capital formation at approximately 24–25 percent of GDP, materially higher than Germany and the United States, which typically ranges between 20–21 percent (World Bank, OECD). More importantly, the composition of that investment has shifted in ways that are strategically consequential for foreign firms.

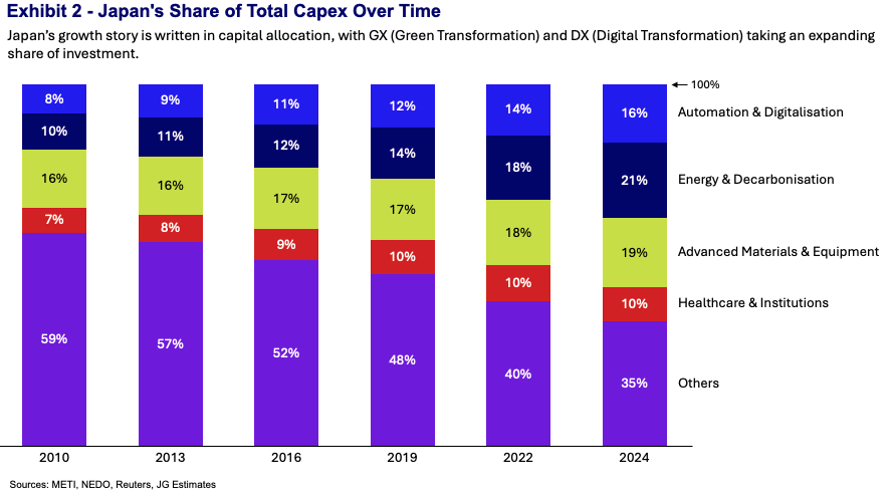

According to Japan’s Ministry of Economy, Trade and Industry (METI), capital expenditure growth over the past decade has been disproportionately concentrated in:

· industrial automation and digitalisation

· energy infrastructure and decarbonisation-related systems

· advanced materials and high-spec manufacturing equipment

· healthcare and institutional capacity upgrades

These are not cyclical investments responding to short-term demand. They are deliberate responses to structural constraints that Japanese organisations are actively engineering around. Once approved, such investments tend to anchor supplier relationships for many years, often across multiple investment cycles.

For CEOs, the implication is not simply that Japan is investing structurally. It is that capital is now being channelled into a small number of defined growth domains where spending is durable, procurement is institutional, and early positioning matters.

The following sections examine three of these domains in detail, where capital commitments are already visible and where Western capabilities are most likely to find sustained demand.

Advanced materials and specialty chemicals are central to Japan’s long-term industrial strategy, particularly as energy systems evolve and performance requirements tighten. Within this sector, hydrogen-related applications are emerging as a critical demand driver, though not the sole one.

Japan’s revised Basic Hydrogen Strategy (2023) targets approximately 12 million tonnes of annual hydrogen consumption by 2040, with deployment across power generation, steelmaking, mobility, and industrial heat (METI). Public and private investment commitments span multiple decades, reflecting Japan’s view of hydrogen as infrastructure rather than an experimental technology.

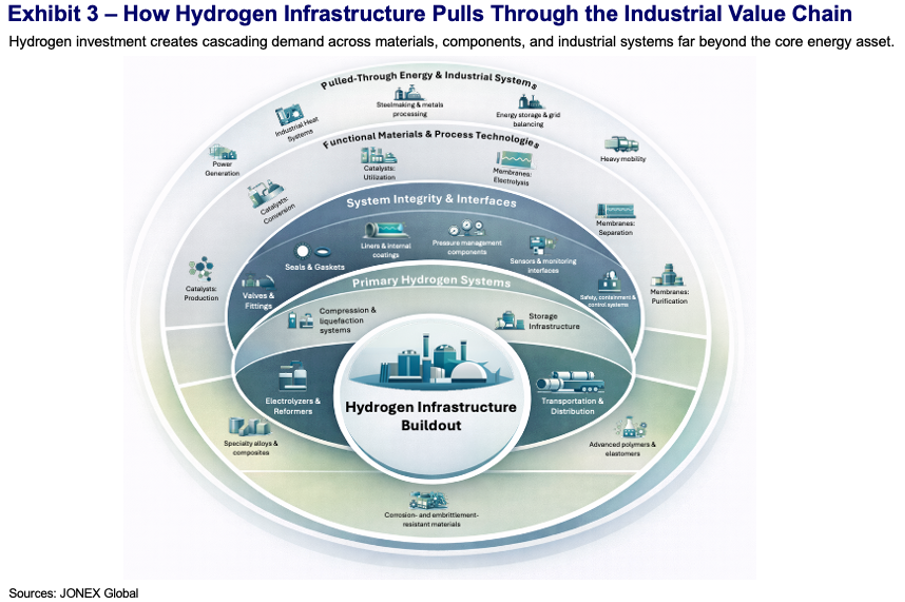

Hydrogen environments place extreme demands on materials. Research by the International Energy Agency (IEA) and Japan’s New Energy and Industrial Technology Development Organization (NEDO) highlights hydrogen embrittlement, permeability, chemical degradation, and long-term fatigue as major failure modes in pipelines, valves, storage systems, and processing equipment.

As a result, demand is rising for:

· Hydrogen-resistant polymers and elastomers

· Advanced barrier coatings and liners

· Specialty composites for tanks and transport systems

· Catalysts and membranes for hydrogen production and utilisation

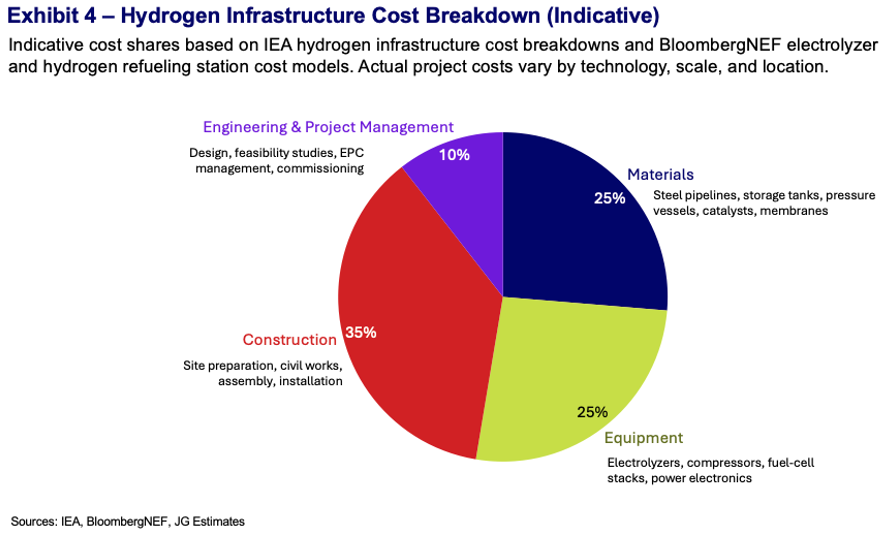

BloombergNEF estimates that materials-related components account for 20–30 percent of total hydrogen infrastructure system costs, with the fastest growth in high-performance specialty materials. Global hydrogen-adjacent materials markets are projected to grow at low-to-mid double-digit CAGRs through 2030, driven disproportionately by Asia and Europe.

Western companies often hold strong positions in precisely these niches, particularly where deep material science, application-specific engineering, and lifecycle validation are required. Importantly, hydrogen acts as an anchor application, pulling through adjacent materials demand in energy storage, industrial sealing, and advanced manufacturing equipment. For CEOs, this sector rewards early ecosystem positioning, technical credibility, and patience through long qualification cycles.

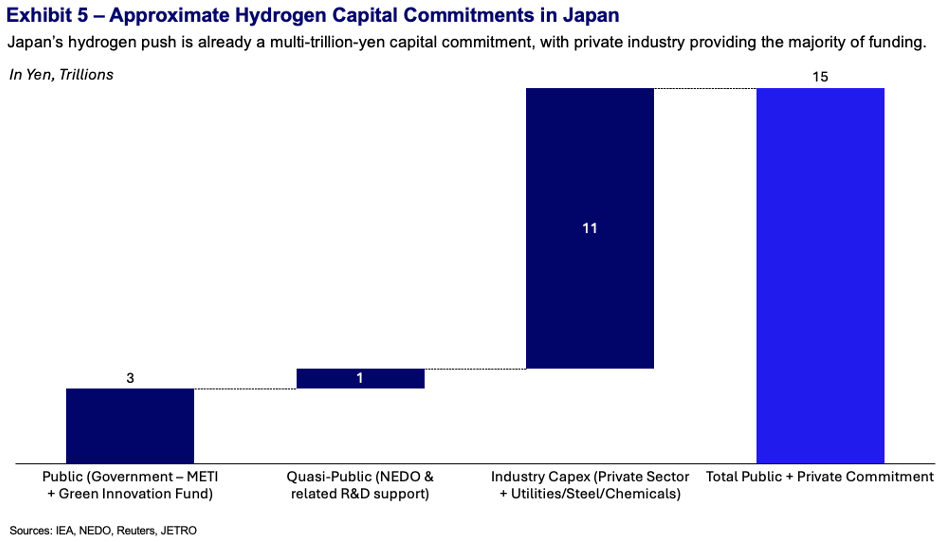

Japan’s hydrogen strategy is backed by large-scale, committed capital, not exploratory pilots. METI has earmarked approximately ¥15 trillion (around USD 100 billion) in public–private investment through 2030 to build out hydrogen supply chains, covering production, transport, storage, and utilisation infrastructure (METI, GX Basic Policy, 2023). In parallel, NEDO has allocated hundreds of billions of yen to hydrogen-related materials, catalysts, membranes, and long-term durability testing, with many programs designed on 10–15 year horizons.

Industrial capital is moving alongside public funding. Major Japanese groups across steel, chemicals, heavy machinery, and utilities have each announced ¥100–500 billion-scale capex programs to upgrade plants and equipment for hydrogen compatibility. A meaningful share of this spending is directed toward materials retrofitting and replacement in pipelines, valves, tanks, seals, and coatings, where existing materials often fail under hydrogen exposure.

For Western CEOs, the key point is timing. Capital is being committed before standards are fully finalised, creating early supplier qualification windows, long lock-in cycles for approved materials, and high switching costs once infrastructure is operational.

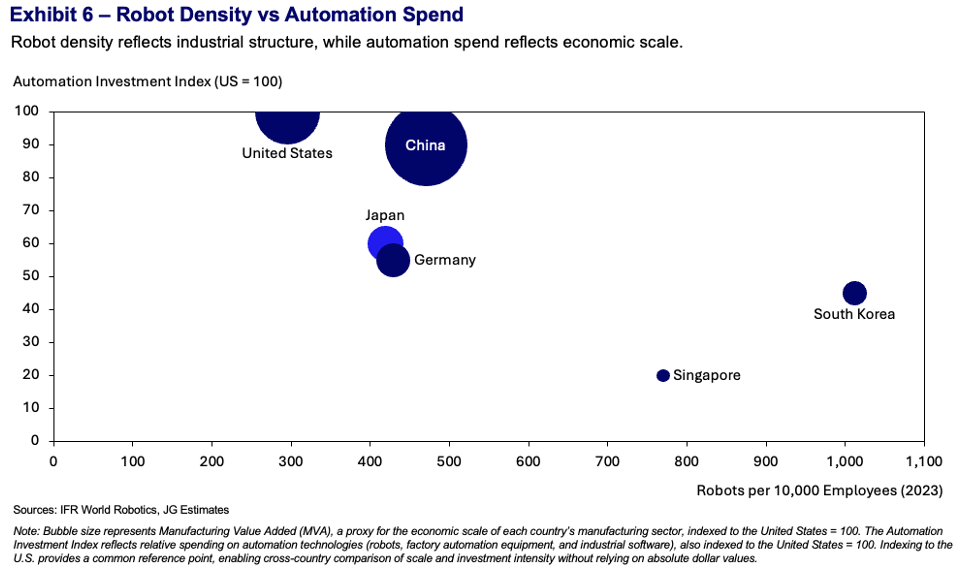

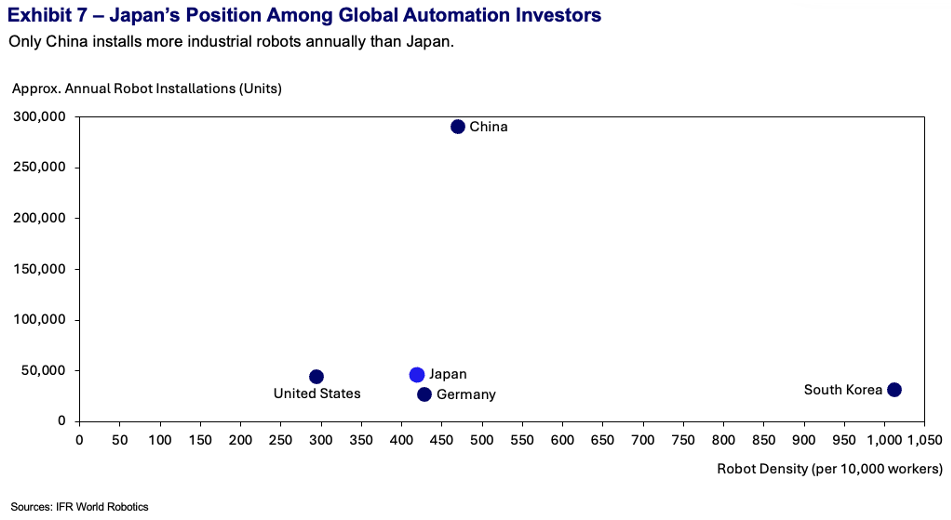

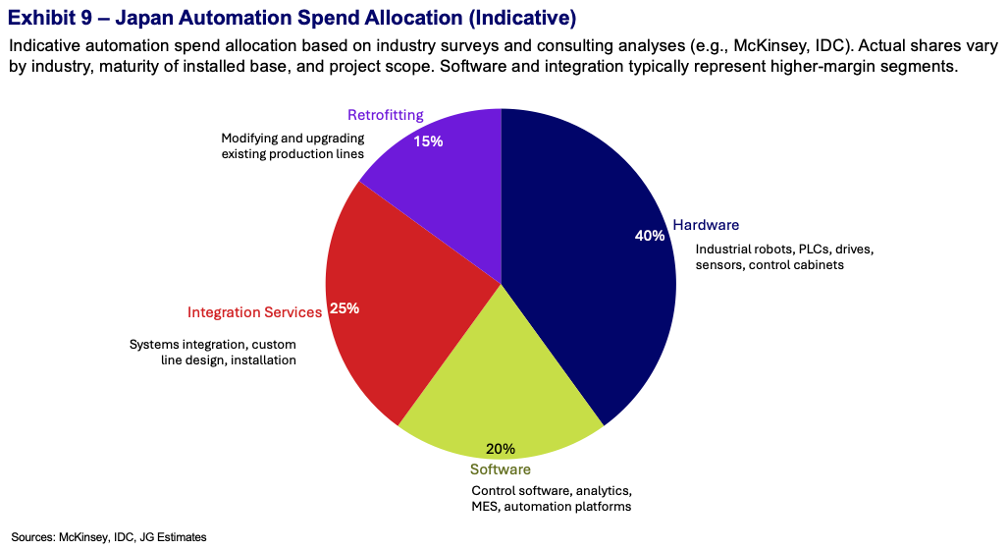

Japan is already one of the most automated manufacturing economy in the world, with approximately 400 industrial robots per 10,000 manufacturing employees, compared with around 300 in Germany and fewer than 300 in the United States (International Federation of Robotics, IFR). Yet automation investment in Japan continues to rise.

This is because automation is no longer viewed primarily as a productivity lever. It is a business continuity strategy.

METI estimates that Japan’s manufacturing workforce will shrink by approximately 15 percent by 2030, while logistics and construction face similar pressures. In response, capital expenditure is increasingly directed toward systems that stabilise output, ensure quality consistency, and reduce operational risk rather than simply lowering unit costs.

While Japanese firms dominate robotics hardware, capability gaps persist in:

According to METI and private-sector surveys, SMEs account for over 99 percent of Japanese firms but lag significantly in automation adoption, creating a structurally attractive segment for solution providers.

Western companies that complement Japanese hardware excellence with software, integration, and adaptability are often well received, particularly when positioned as long-term partners rather than disruptors.

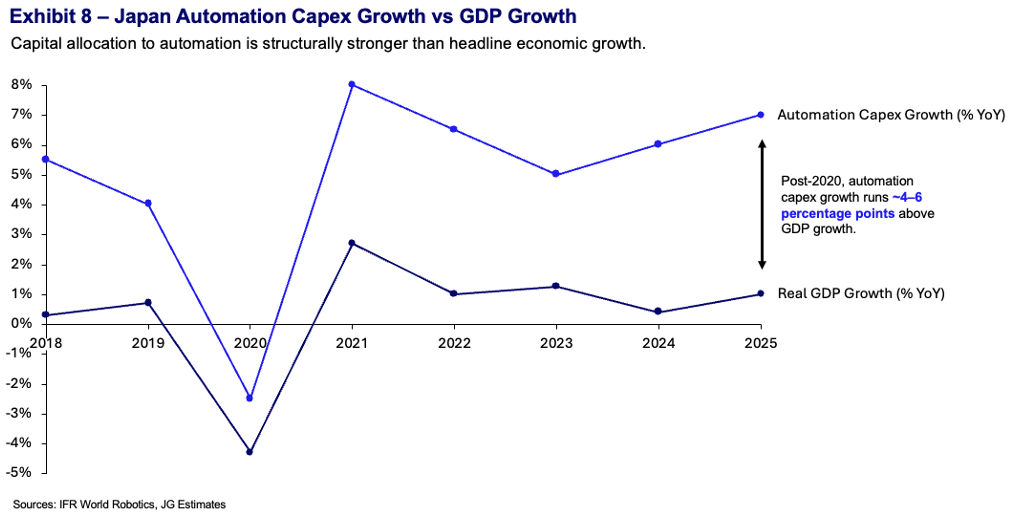

Automation investment in Japan is no longer discretionary innovation spending. It is increasingly replacement capital required to sustain output and operational reliability. According to METI, automation and digitalisation-related manufacturing capex has grown at approximately 6–8 percent CAGR since the mid-2010s, even during periods of flat GDP growth. In absolute terms, Japan consistently ranks among the top three global markets for industrial automation investment, not only by robot density but by total capital deployed (IFR, OECD).

At the enterprise level, large manufacturers now allocate double-digit shares of annual capex to automation, control systems, and factory modernisation. Among SMEs, capital deployment is further accelerated by government programs that subsidise 30–50 percent of automation investment, materially lowering adoption barriers and protecting budgets.

Importantly, a significant share of automation capex is directed not toward hardware, but toward software, systems integration, retrofitting, and engineering, areas where Western firms often hold structural advantages. For Western CEOs, the implication is that automation budgets in Japan are recurring, operationally protected, and relatively insulated from economic cycles, making the market lower risk than headline growth metrics suggest, despite longer sales cycles.

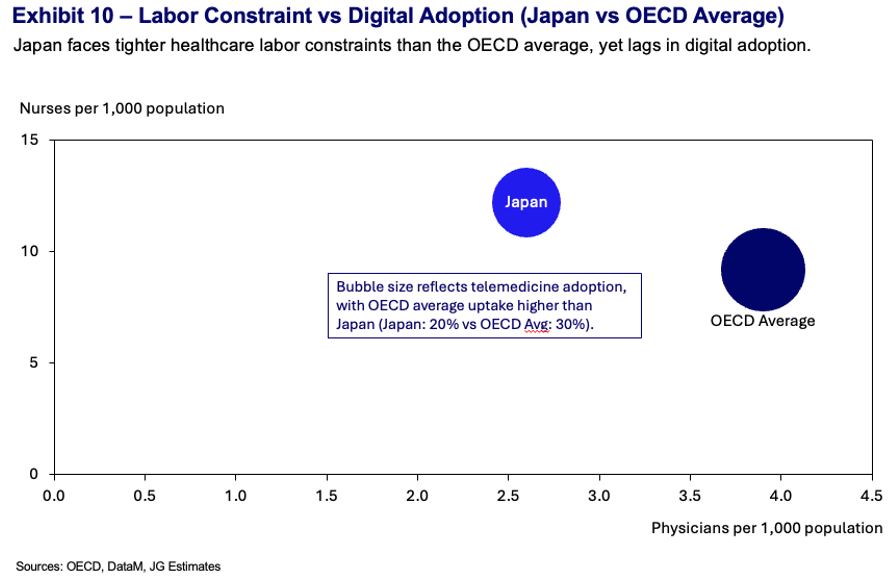

Japan’s healthcare system is highly developed and well-funded, with healthcare spending at approximately 10.9 percent of GDP, comparable to Western Europe (OECD). The binding constraint is not funding, but capacity.

The Ministry of Health, Labour and Welfare (MHLW) projects a shortfall of up to 690,000 healthcare workers by 2030, even under conservative demand scenarios. As a result, investment is increasingly focused on technologies that reduce labour intensity per patient and improve system-level efficiency.

This is driving adoption of:

Japan’s digital health market is projected to grow at high single-digit to low double-digit CAGRs through 2030, with strongest demand from hospitals, long-term care providers, and municipal health systems.

Western companies often bring strengths in software platforms, interoperability, and user-centric design, areas where Japan’s healthcare IT ecosystem remains fragmented. However, success requires rigorous regulatory alignment, extensive validation, and trust-building with institutional buyers. For CEOs, digital health in Japan is best understood as a long-horizon institutional market, not a venture-style growth play.

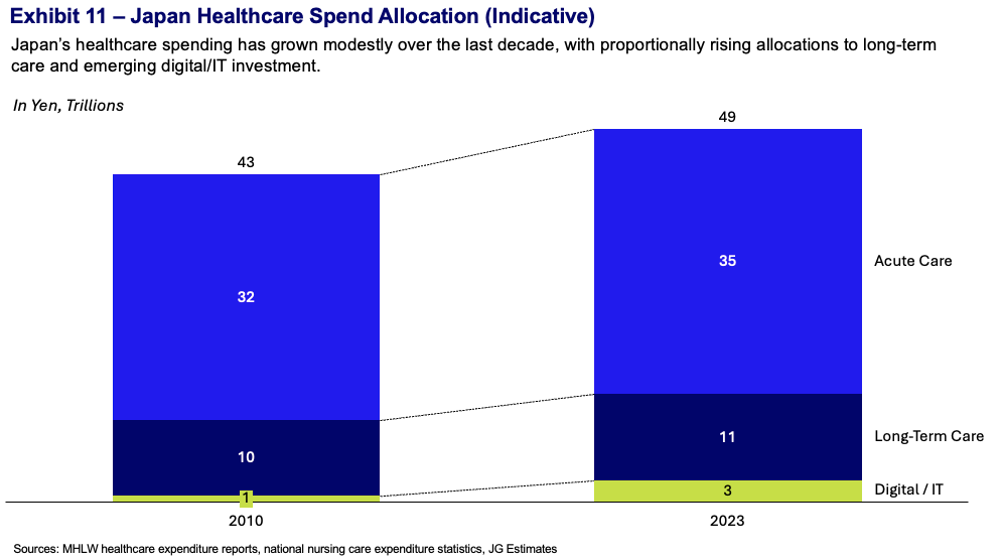

Digital health demand in Japan is being driven by budget reallocation within existing healthcare systems, not by experimental or venture-led spending. Japan’s healthcare system deploys more than ¥45 trillion annually (approximately USD 300 billion) in total healthcare expenditure (MHLW), and within this envelope, the government has explicitly earmarked multi-year budgets for digitalisation, workflow optimisation, and remote care, particularly at hospitals and municipal care providers.

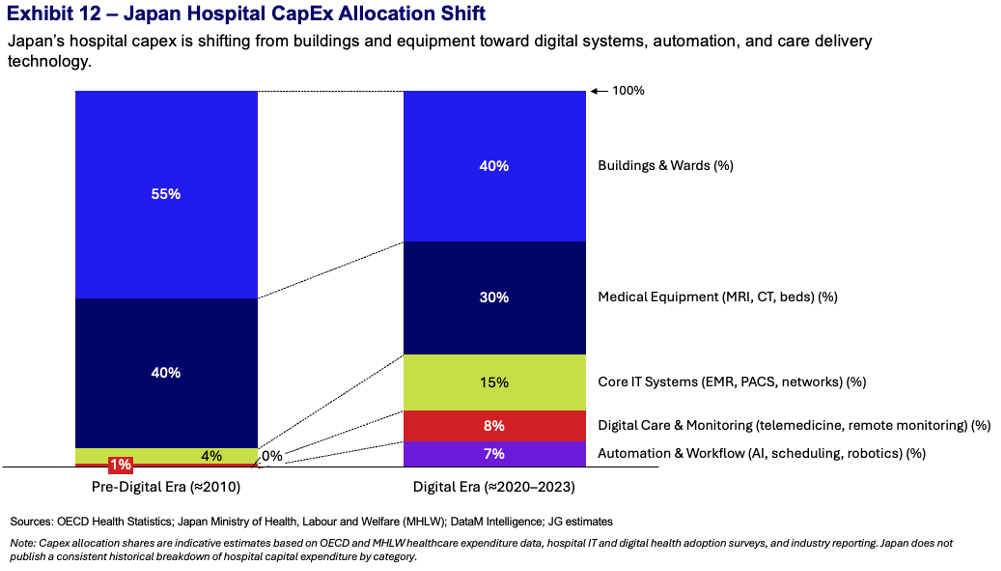

At the provider level, large hospital systems are increasingly allocating capital toward electronic medical record integration, remote monitoring infrastructure, and care coordination software. These investments are often embedded into facility upgrade and modernisation capex, rather than treated as standalone IT pilots, which materially increases adoption durability.

Private research and MHLW-linked projections estimate Japan’s digital health segment growing at approximately 8–12 percent CAGR through 2030, despite flat overall healthcare spending. For Western CEOs, this signals a market characterised by institutionally budgeted, procurement-driven, and recurring demand. Entry timelines may be longer, but once embedded, customer lifetime value is typically high and resilient.

Japan’s headline macro indicators obscure a deeper strategic reality. Capital is being deliberately reallocated toward sectors that sustain industrial output, secure energy systems, and preserve institutional capacity. These investments are conservative, long-dated, and increasingly open to foreign participation where capability gaps exist.

For Western CEOs, several priorities stand out:

· Japan should be treated as a strategic anchor market, not a tactical growth initiative. Its value lies in durable demand, high lifetime customer value, and global signalling power as a reference market.

· Leadership teams should prioritise value density over volume, focusing on fewer customers, deeper integration, and higher specification requirements.

· Offerings must align with structural constraints, not trends. Labour availability, energy security, and institutional scalability are enduring realities that anchor demand regardless of economic cycles.

· Companies should invest early in credibility, validation, and ecosystem positioning, accepting longer front-end timelines in exchange for more stable long-term returns.

· Finally, Japan requires a distinct operating model, with clear authority, realistic timelines, and commitment at the senior-most levels

For Western companies prepared to align with these realities, Japan is not only a source of growth. It is a source of enduring strategic advantage.